The Jews newly arriving in Stühlingen, having been expelled from the cities, were not permitted to own and operate farms, were barred from the craft guilds, and were hobbled by a variety of restrictions in their letters of protection. Their first priority had to be to establish an economic base to meet their hefty tax burden, to support themselves and their families, and to maintain their community institutions.

Rural populations tend to be inherently reserved towards outsiders in general,1 and in the seventeenth century were outright hostile to the manifest “Christ killers” in particular.2 It is remarkable that the Jews were able, under such adverse conditions, to find an ecologic niche not only to survive but even to flourish. The only possible way for them to succeed was by providing added value over what was already locally available. In other words, Jews had to plug an existing gap in the rural market economy. In the following study, we will explore the nature of seventeenth-century rural market economies in southern Germany and identify gaps. We will examine the skill and tool set Jews brought with them to match these gaps. Finally, we will survey the nature of the solutions Jews brought to market deficiencies in early modern Stühlingen.

Starting in the Stone Age, hunter-gatherers evolved into self-sufficient subsistence farmers. With growing skills and technological progress, some managed to produce excess over their daily need; but what to do with the surplus? They could exchange it for luxuries, for implements to further increase their productivity, or they could shelter it in suitable form for a rainy day. It took society centuries, if not millennia, to figure out how to render this exchange process efficient. At first glance, barter seems to provide the solution: I give you my surplus, and you give me what I want or need! But what if I can spare a basket of apples but need a cow? Or, I have the apples now, but your cow needs to give suck to a calf for the next three months. In the words of the renowned nineteenth-century British economist William Stanley Jevons:

“Barter suffers from three serious inconveniences: a want of coincidence of needs, a want of measure of value, and a want of means for subdivision”3

Maybe this problem could be solved with some tokens serving as intermediaries. But what would keep enterprising individuals from simply producing the tokens? The tokens needed to be linked strongly to the value of goods against which they could be exchanged. In other words, it should not be cheaper or easier to produce the tokens than to produce the corresponding goods. The Babylonian Code of Hammurabi already referred to unminted gold as value intermediary around 1750 BC.4 Coins appeared around 700 BC.5 The value of these exchange tokens – which we can now refer to as money – was guaranteed by the scarcity of their base material. Paper money was invented under the Chinese Sung dynasty in 1024 AD and continued by the Mongol regime of the Yuan dynasty.6 Its value was supposedly guaranteed by a powerful state but still succumbed periodically to issuing excesses and forgery.

Germany did not become a unified nation until the nineteenth century. Before that time, it consisted of a loose federation of more or less autonomous kingdoms, duchies, and counties, all subject to the emperor of the Holy Roman Empire of Germany. Many of these states minted their own coins, some in similar, some in different currencies. But even two coins of the same denomination could differ in value, depending on where they were minted.7 The value of coins varied over the years because the metal was debased or the size was clipped.8 Germany did not introduce paper money until the late nineteenth century. Doing business in cash was a challenge for the seventeenth-century peasant. Even if he actually owned sufficient money, it was often in mixed currencies and denominations. It took expertise to determine the exchange value of a purse’s content,9 and carrying a large sum could be a back-breaking task.

The nominal currency in seventeenth-century Stühlingen was the florin (fl.), originally a gold coin minted in Florence from 1252 to 1533 as the fiorino d’oro (little flower of gold), named after the prominently embossed lily flower on its reverse. The florin was produced in sufficient numbers to function as a leading currency all over Europe. Subsequently, it was copied in many countries in order to support market economies. In Germany the best known of these copies was the Rhenish florin, or florin of Four Electors of the Rhine (Gulden), minted from 1354 on.10 Unfortunately, Florentine bankers previously had also introduced a silver florin, or fiorino grosso, in 1237.11 A gold fiorino originally was worth 20 silver fiorini. This silver fiorino eventually became the florin of account, or affiorino.12 Many account books recorded moneys in florins, independent of the currencies and coins in which the business was transacted. In fact, the florin proper is not even listed among the popular, historic coins used in Stühlingen.13

Jevons’ initial criticism of the inconvenience of barter might also be read somewhat differently: “I require some goods now, but I will only have the means to satisfy the needs of their current holder in the future.” In these cases, money will not do as an intermediate token. The corresponding transaction sounds suspiciously like a loan, which may be secured by a movable (pawn) or unmovable (mortgage) object. But why would anybody loan his money to somebody else? After all, while the money is loaned out, the owner is deprived of its use and even risks losing it. Yet, the Torah obliges the just to lend his money to the poor members of his people and prohibits the taking of interest, although collecting interest from strangers is permitted.14 Both the New Testament and the Koran scorn interest based loans altogether.15 Money lending represents not only a moral but also a practical issue. Without a positive incentive for money lending, a society’s economic activity will be severely curtailed. All Abrahamic religions have seriously struggled with this thorny problem over the centuries. And all have ultimately found solutions, sophistic in their justification and pragmatic in their application.

Instead of real money, a certificate issued a by trustworthy person or body guaranteeing its exchange value would fit the bill. One of the first-known such instruments was a draft issued by “The Guarantor at Elephantine-Syene.”16 It is among the so-called Elephantine papyri, a collection of ancient Jewish manuscripts dating from the fifth century BC found during excavations on Elephantine Island in the Nile on the border between Egypt and Nubia. By shifting the guarantee of the letter from its bearer to a known and respected independent entity, the receiver is more likely to trust and honour its value. But it all rests (i) on the trustworthiness of the issuer and (ii) on the authenticity of the instrument.

Such drafts gradually evolved into what are now called “Negotiable Promissory Notes.” The literature places their early appearance in twelfth-century Genoa.17 A variant, namely the “Negotiable Promissory Note Payable to the Bearer on Demand” (also known by its Hebrew acronym MaMRaMe) turned into the favourite financial instrument of Jewish merchants by the sixteenth century.18 Simply put, the issuer of the certificate promises its bearer a sum of money to be repaid at the bearer’s request. The great feature of the MaMRaMe was its validity both in external gentile and in internal Jewish business transactions. Thus, the certificates could be issued, held, sold, or bought independent of one’s dogmatic frame. They turned into a money substitute when the real thing was not available.

In Stühlingen, this instrument was simply called “claim” (Forderung). Once its nominal value exceeded a certain threshold, it had to be registered with the authorities; this registration and the associated increased trustworthiness of the claims added further to their wide acceptance. Claims were always valued in florins. Our data set mentions 1880 such claims over the 139 years from 1604 to 1743. Credit, prior to the arrival of Jews, was not unknown in rural Germany. Merchants might allow customers some payment delays. Similarly, some landlords showed flexibility in the collection of their rents.19 The church too occasionally provided mortgage funds [R3557]. Property could be converted to income streams through annuities (Renten).20 But “claims” had the double advantage of being easily available and flexible, almost like today’s credit cards.

Serfdom had been abolished in western Germany by 1600. The policies of West German princes had encouraged an entrenched landholding peasantry, so that in the period under discussion the peasantry had taken hold of up to 90% of arable land.21 The people who make up an agrarian workforce are commonly designated as peasants or farmers. But this designation is very imprecise, since it includes a varied group of people with a wide spectrum of wealth, skills, and status. Statistical ensembles can change easily over time and place, a fact that clouds the validity of any generalization.22 Peasants could be subdivided into two major groups: those who owned the land they tilled and those who did not. Among the former were the wealthy owner/operators of large contiguous family farms and the smallholders, the latter often with fragmented holdings. The landless included farm workers who worked for wages and tenants who leased the land against a share of their harvest.

Much of the Black Forest landscape is rugged and suited more for small farms than for large contiguous family farms. The famines of the sixteenth century had left the German peasantry impoverished,23 at best leaving only a small surplus of production over consumption. Economic pressures in the late sixteenth and early seventeenth century gradually tended to segregate agrarian society into two layers: by 1581 the bottom 80% who collectively owned some 40% of the wealth, and the top 20% who owned the other 60%.24 The large contiguous family farms at the top in general were successfully handed down intact to the next generation, while the small properties tended to be constantly fractured and redistributed.25 In contrast to the margraviate of Burgau,26 the Stühlingen region lacked a significant, export-oriented textile production, although the town featured small dyeing and pottery manufacture.27 The town had its complement of tanners and tawers, bakers and barbers, as well as several inns, but the region’s economy was based mainly on agricultural produce. Stühlingen featured its own public market hall, in which Jews too were allowed to trade.28 But most likely it served only as retail market (Latin macellus publicus), supplying residents with their basic needs.29 Up until 1659, the town would hold three annual fairs; two more were added that year.30 But the Stühlingen fairs paled in comparison to the bi-annual Zurzach fair, thirty kilometres to the southwest in Switzerland.

understanding of business matters. They were familiar with sophisticated credit instruments and accounting, were literate, numerate, and able to keep business records. While some may have arrived bearing a reasonable starting capital, most probably did not. Those who came from cities had little knowledge of animal husbandry or the idiosyncrasies of agricultural products, and had no access to merchandise supply chains. They literally had to live on their hooves, which they did largely by providing the “economic yeast” that helped the market economy to rise.

The personal transaction ledger formed the core of a rural Jewish merchant’s business practice. In fact, it was more valuable than gold or silver:

After Isak of Stühlingen [B1] had escaped from Conrad of Pappenheim in 1599 and fled to the little town of Aach, his son Mayer [B1.1 together with a granddaughter were visiting Isak’s elderly wife in Stühlingen. As they were about to leave, the mother started crying disconsolately. She felt unable to handle all the debtors and creditors who had business with her husband. So Mayer and his daughter packed the account books in a little wooden case to take them to Isak. Mayer and his daughter were promptly arrested by Pappenheim’s sheriff on the way. The count was furious that no tangible valuables were found, and incarcerated Mayer for almost two years.31

As recorded through the lens of the seventeenth-century municipal court, today it is very difficult to interpret these business books. Furthermore, little agreement exists between parties in question as to who paid what when and how. For example, on May 16, 1652 Menckhe (C2.1.2) claimed 164 fl. capital plus another 50 fl. for a field on behalf of his father Mayerle (C.1) from the cooper and tub maker Hans Bühlmann of Eberfingen, a claim that originated in 1637. Bühlmann, on the other hand, admitted a debt of only 170 fl., including the field. Menckhe insisted that his books were correct but was willing to inquire of his brother Eli (C1.2.1), who was keeping the book. On that basis, both parties were willing to base the account tentatively on the admitted 170 fl. Let us inspect the court transcript [R1907]:

| Explanation in document | fl. | Comment by author |

| Amount owed | 170 | Agreed upon amount (120fl. + 50fl.) |

| Accumulated interest | 72 | 4.5% simple interest on 120fl. for 16 years |

| Subtotal | 242 | |

| Payments rendered | -26 | Both parties agree that these payments were made. |

| Subtotal | 215 | |

| Transfer of a claim | -30 | Probably an outstanding claim of Bühlmann as payment |

| Payment to the church in Eberfingen | -5 | Unclear why such a payment should be deducted from debt |

| Subtotal | 180 | |

| Interest on remaining for 1650/1 | 9 | Corresponds to 5% on 180 fl. (1 year) |

| Subtotal | 189 | |

| Menkhe demands capital | 8 | No explanation |

| Interest on 8 fl. for 21 years | 9 | Simple interest at 4.5% |

| Total debt in 1653 | 207 | 1 fl. discrepancy |

Finally, Menckhe and Hans Bühlmann settled for a total payment of 160 fl. Of this total 100 fl. were to be paid in 1652 and the rest plus applicable interest subsequently in tranches of 10 fl. per year. The questionable 44 fl. were to be reviewed again, once the answer from Eli was received. The transcript suggests that both logic and arithmetic were fuzzy, and there was always room for compromise.

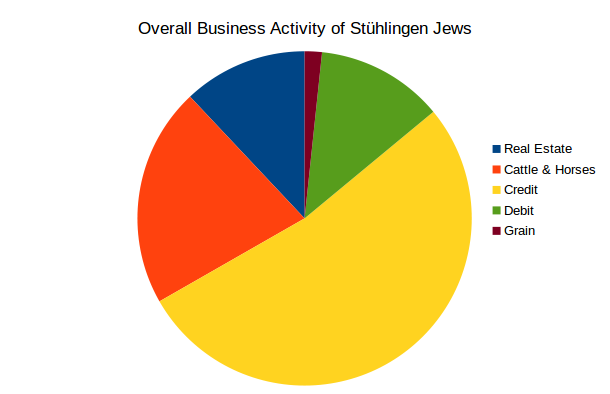

But rather than focusing on individual transactions or merchants, let us examine the overall commercial pattern of the Stühlingen Jews, based on the abstracted records (fig. 7). These records mainly mention just the fact and character of a transaction without providing its numeric value.

Among the 4826 collected records, we identified 2630 commercial transactions involving 131 Jewish merchants. Because of the nature of the records, we simply counted the transactions according to type, independent of their value. We found 1387 credit records, 324 debit records,32 559 cattle and horse deals, 316 real estate deals, and 44 grain transactions. The relatively small part the grain trade played in the business spectrum of the Jews may appear surprising at first glance. But the requirement for a hefty infrastructure for transportation and storage, largely barred to them, may offer a plausible explanation. We have to accept that the initial recording of transactions was probably incomplete, that documents may have been lost over the intervening three hundred years, and that the data capture from the archives was incomplete. The data set available for analysis thus constitutes only a sample from the universe of business deals transacted by the Jewish merchants of Stühlingen between 1604 and 1743. We have no reason to suspect deliberate bias. But we do not know the threshold value above which transactions had to be recorded. We may have slightly oversampled cattle and horse deals because they seemed to have given rise to legal repercussions more frequently than other types of transactions; the reason for this will be discussed later.

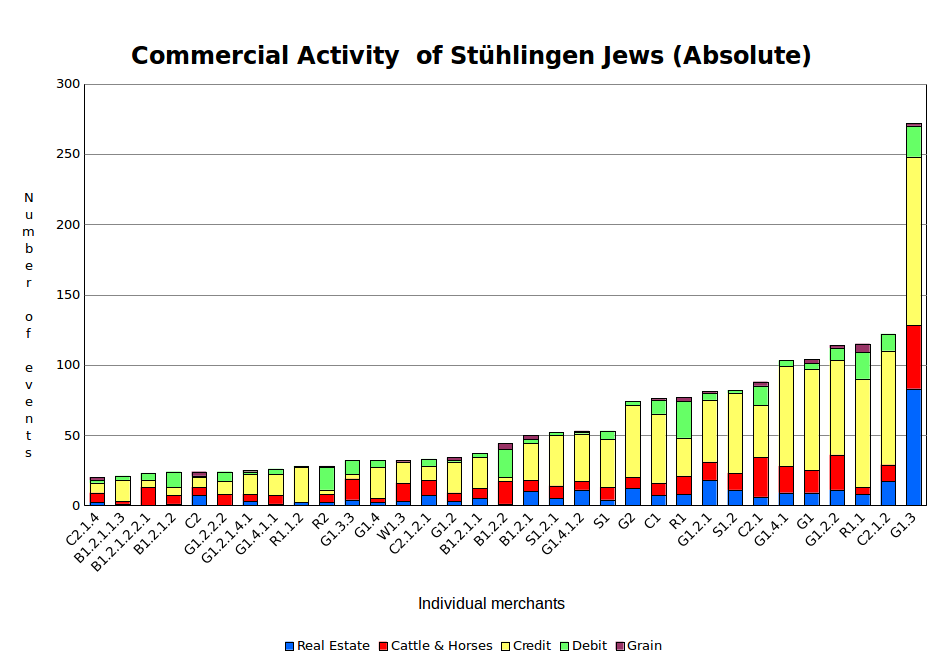

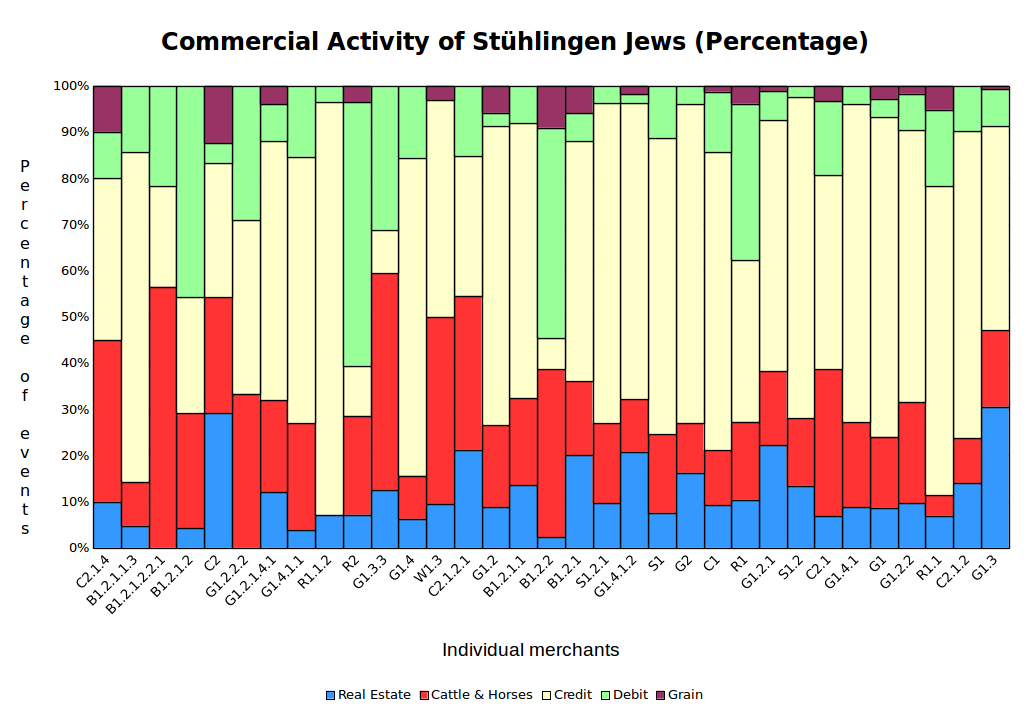

Since we are primarily interested in patterns of economic activity rather than individual performance, only every second merchant is labelled by his identifier. From figure 8 it is quite evident, that one merchant Marum Gugenheimb (G1.3), Jekoff’s son, who was active from 1632 on and died in 1685/6, sticks out from the crowd. He must have had a special knack for business and appears quite prominently in Peter Stein’s attempt at reconstructing the Jewish community of Stühlingen.33 But because of Marum’s dominance, figure 8 is not suitable for comparing the business spectrum of individuals. Figure 9 shows the same data but in a relative representation. In this graph, we can now see that the merchants all employed practically similar patterns of business mix.

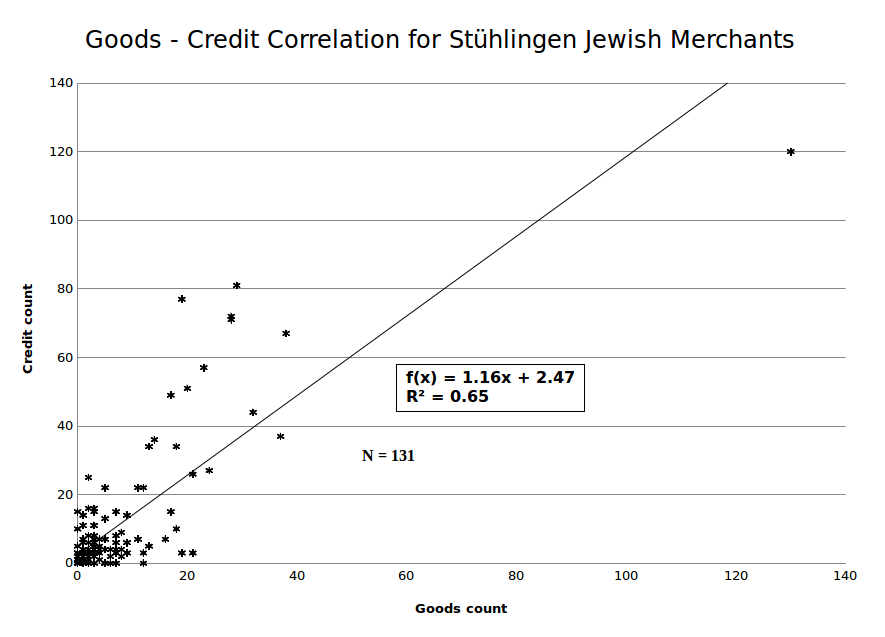

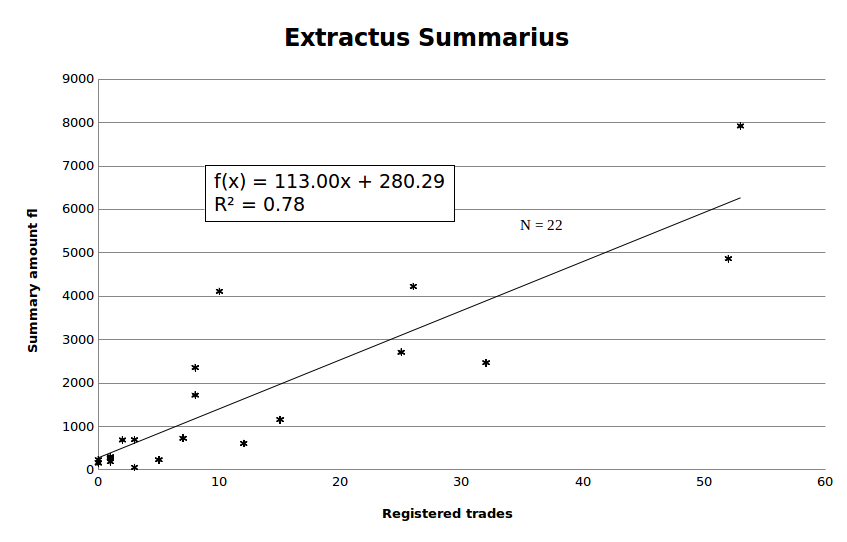

Merchants (R1), (B1.2.2), (R2), and (B1.2.1.2) had a markedly higher frequency of debts than the rest. But rather than just eyeballing the similarity between the merchants, we can use a statistical method called Pearson Product Moment34 to compare the patterns of the full 131-merchant sample. According to this method, for each merchant we plot the sum of grain, cattle and horse, and real-estate deals on the x-axis against their number of owed claims on the y-axis (figure 10).

Figure 12 again shows a statistically highly significant association between the number of sales enacted and the total amount of claims due. In other words, the amount of money owed to a Jewish merchant was directly proportional to the number of his sales. It appears that the Jews listed in the Extractus summarius were neither moneylenders nor merchants; instead they plied an integrated business, with their claims being nothing else than accounts due. The comment accompanying the document, describing the reason for the magnitude of credits as:

“the vicious, double-dealing and fraudulent purchase, barter, credit, and other contracts against the poor inhabitants who had to seek the assistance of the Jews out of necessity and poverty,”38

amply illustrates the attitude of the princely house and its administration. But the governor’s (Obervogt) verdict granting the population sixteen years to the repay the loans presents a strong argument that the credit system provided by Stühlingen’s Jews constituted a significant component of market capitalization in the local economy.

Cattle dealing in the early modern period is readily comparable to today’s used car market. Buyers were trying to get as cheap a deal as possible, and they easily felt cheated when the goods turned out to be defective. Isaac (B1.2.2) was sued because a horse he had sold dropped dead soon after [R3174]. But liability could also be taken too far: Marumb Jekhoff’s son (G1.3) was sued for a horse that he had sold eighteen years earlier [R3852].

Jews also traded in prime goods: “Jägglin Jew sold a horse, which the prince took to Bohemia, for 84 fl.”[R34]. Many other types of assets could serve as security:

Jerg Hoz and his stepmother demand the return of a ploughing harness from the heirs of Jekhoff (G1) that had been deposited as pawn sixteen years earlier. Jonas Jew (G1.4), Jekhoff’s son, responded for himself and his brother Marumb (G1.3) that they were not aware of this matter and had to look it up in their books. They were also going to consult with their brother (G1.1) in Lengnau [R1889].

Jewish business books probably contained amounts written in Indo-Arabic numerals, but the text was in Yiddish spelled with Hebrew letters. The Stühlingen records describe at least nineteen incidents where Jewish merchants had to present their business ledgers in court, either as plaintiffs or as defendants to argue their case. Receipts too often bore inscriptions in Hebrew letters. In such cases, the courts could either accept the writer’s testimony or call a trustworthy Jew as expert translator [R1401].

Some degree of specialization existed among the merchants. Lemble Weil (R1.1.1), who initially had traded in the full spectrum of goods allowed to Jews, by the 1690s sold mainly nails, cloth, linen, silk, and ribbons [R113]. The Jews also did business with the count’s court. Some were straightforward sales and purchases of horses [R1014]. But in 1619 the Jews collectively gave a loan of 100 fl. to the dominion, of which 10 fl. was used to pay off a loan to Jeggle (C2) and 90 fl. to the mason for the reconstruction of Castle Hohenlupfen [R1517]. Another transaction illustrates the whole complexity of the credit instruments:

Hürzel (B1.2.1) sells a claim of 30 fl. for 24 fl. to the dominion from which he uses 14 fl. for his own protection fee and 10 fl. for the protection fee of his stepbrother Jeslin Jew” [R1509].

Claims were thus discounted and/or traded like cash. Some of these claims had a very long validity. Marum Tochtermännlin (S1) wanted to collect a twenty-eight-year-old claim in 1660 [R3821]. Some debtors owed money to as many as eight different merchants: “Claims against Hanns Rebmann called Gussi: Jäggle Jew (C2) 134 fl., Hürtzle Jew (B1.2.1) 60 fl., Meierle Jew (C2.1) 8 fl., Jecoff Jew (G1) 8 fl., Cost (R2) 1 fl., Isaac (B1.2.2) 4 fl. + 3 fl., the heirs of Sannel Jew(C1) 15 fl., Judele Jew of Ofteringen (O4) 30 fl. + 5 fl. [R1654].

Claims were also used like cash. In 1684:

Meyerlin, Menkhin’s son (C2.1.2.1) passed a claim to his sister, who had just married [R1358].

Estates were frequently settled in claims as well:

“Jeckoff (G1.2.2.2) has inherited a claim from his father Callmel." (G1.2.2)”[R955]

And similarly:

“Marumb (G1.3) and Jonelle (G1.4) Jews, Jeckhoff´s (G1) sons and heirs, ledger. The following participate in the claim: the heirs of Schmul (G1.2) Jew (22 fl.), Marumb (G1.3) Jew, Jonas Jew, and the heirs of Josephle (G1.1) Jew (38 fl. each) [R2112].

But credits did not have to be heartless. The Stühlingen protocols record a deposition:

Christa Fössler and his wife in Schwaningen are grateful to Jew Sandel (S1.2). Since he did not aggressively pursue his interest at their bankruptcy, they were able to keep their farm. As the Jew lost about 150 fl., they assigned him a mortgage of 50 fl. beyond the court settlement [R3720].

In fact, while the crimes and misdemeanours of Jews occupied the courts quite frequently, not a single accusation of or conviction for usury was among the 622 cases concerning Jews.

Jews were not only lenders; they also borrowed money for leverage. With the general cash shortage in the country, the major lenders were in the cities: “Treasurer [Säckelmeister] Hurter of Schaffhausen claims 202 fl. from Jägglin Weyl Jew (R1.1) in Stühlingen. The claim originates from 1640 [R3921].

Business ethics of the Jews likely spanned the entire spectrum between honesty and outright fraud and theft, although acts of rectitude are unlikely to be found in court proceedings and municipal records. The worst case probably involved organized cattle rustling:

Veit Weihl (U1.2) Jew, who has lived in Stühlingen dominion for a while and most recently in Donaueschingen dominion, is sued for payment of 69, 51, and 64 fl. for horses. His protection in Donaueschingen was annulled, and he is on the run. The stables of Jews Jäckle (C2.1.4), Joseph (G1.3.3), Marumb’s son, and Judele (U1.1), Veit’s brother, were inspected, and the horses were found. Plaintiffs can get their horses back if they present evidence that they are the owners. The wife of Veit Weil had arrived with a little child last night, heading for Lenglau [Lengnau] as he [Veit] had ordered her to go [R1356].

The purchase and sale of stolen goods was not uncommon. The records for the period of 1604 to 1743 show thirteen accusations or convictions for trading in stolen goods. These crimes contravene not only the laws of the land, but knowingly trading in stolen goods is also clearly forbidden by the Halacha.40

In 1629 “Davidt Jew of Eberfingen (Z1) is fined for buying stolen items” [R1689]. Later on “Lew (G1.4.1) Jew at Stühlingen is fined 6 fl. for buying stolen cloth from some soldiers” [R54], and the same “Lew of Stühlingen is fined 10 pounds for buying stolen property” [R4690]. Stolen goods were also taken as security on loans: “Jäcklein Lehman’s son-in-law in Horheim (M1.1) has taken stolen clothes as a pawn and is fined 10 pounds” [R4785].

In the beginning, Jews could easily buy and sell land and buildings, particularly in the villages and surrounding country. At times, they made a good profit. Things changed in the 1670s due to restrictions imposed on holding land. For example, in 1677 Sandel (S1.2) bought a meadow for 100 fl. and had to resell it for 60 fl. [R4926]. From about 1730 on, most real-estate transactions required a gentile resident to represent the Jewish buyer or seller [R4975]; the reasons for this practice are not apparent. Jews were allowed to own houses in Stühlingen, and often family members shared a building [R804]. Occasionally, a Jew did share a building with a gentile neighbour [R716], but each purchase of a Jewish residence had to be approved by the authorities [R2322].

In 1731 the scope of Jewish trade was further reined in:

The wool weavers complain that Salomon Weyl, Sandels Marumben’s son, is illegally importing woollen cloth from Nördlingen. The Jews respond that according to their letter of protection, they are allowed to trade in any merchandise except steel, iron, and salt. Decision: the Jews are obliged to buy the cloth from the local wool weavers [R2297].

Financial records reveal yet another insight into the economic reality of Stühlingen’s Jews. Marum, Jeckhoff's son, whom we have identified earlier as a super businessman, died around 1686. His widow Mergam tried to carry on the business, but by 1700 she was freed from having to pay protection because of abject poverty [R4454]. There are two possible explanations: (i) Marum’s business model was based on a high degree of leverage and therefore dependent on regular cash flow. (ii) In 1663 Marum countersigned a 680 fl. loan for his father-in-law Marx Hönlin, called Süesskind, in Oettingen [R3946]. Hönlin defaulted, and Marum was left with the huge debt [R4023].

Overall, the Jews of Stühlingen were quite successful merchants. As a group, they probably would not have rated highly with the Better Business Bureau; but they seemed to have provided an integrated business and credit system that helped the rural market to function. As evidence shows, their credits acted almost as substitute currency, one even used by the authorities [R1509].

Footnotes -> List of References

1Malcolm, “Outsiders Within.”

2Perry and Schweitzer, "Anti-Semitism."

3Jevons, "Money and the Mechanism of Exchange", ch. 1.

4Harper, "The Code of Hammurabi."

5Kagan, “The Dates of the Earliest Coins.”

6Chen, Chang, and Chen, “The Sung and Ming Paper Monies.”

7Döring, "Handbuch der Münz-, Wechsel-, Mass- und Gewichtskunde",14–38.

8Shaw, "The History of Currency", 103–5.

9Grierson, “The Monetary Pattern.”

10Munro, “Money and Coinage,”

11Ibid.

12Ibid.

13Häusler, "Stühlingen: Vergangenheit und Gegenwart," 252.

14Cf. Exod. 22:24; Lev. 25:35–7; Deut. 23:20–1.

15Cf. Luke 6:34–5; Al-Baqarah 2:275

16Porten and Greenfield, “The Guarantor at Elephantine-Syene.”

17Rabinowitz, “The Origin of the Negotiable Promissory Note.”

18Katz, "Tradition and Crisis," 58.

19Toch, “Local Credit.”

20Gilomen, “Das Motiv der bäuerlichen Verschuldung.”

21Brenner, “Agrarian Class Structure,”

22Robisheaux, "Rural Society."

23Ibid., 69–79.

24Ibid., table A.3.

25Ibid., 84–9.

26Ullmann, "Nachbarschaft und Konkurrenz" 56–7.

27Häusler, "Stühlingen: Vergangenheit und Gegenwart" 241.

28FFA, Judenakte, Politica, Amt Stühlingen, div. I, subdiv. 1, Die Annahme der Juden 1615–1784.

29Dickinson, “The Morphology of the Medieval German Town.”

30Häusler, "Stühlingen: Vergangenheit und Gegenwart." 221.

31Rosenthal, "Heimatgeschichte der badischen Juden," 462–6.

32Both from the perspective of Jewish merchants.

33Stein, “Die Juden zu Stühlingen.”

37Fontaine, "History of Pedlars in Europe." pp. 8 - 34

39Weldler-Steinberg and Guggenheim-Grünberg, "Geschichte der Juden in der Schweiz," 42.

40Cf. Lev. 19:11.

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.