After the death of Erbmarschall, Count Konrad of Pappenheim, in 1603, his son Maximilian was invested as the new ruler in Stühlingen. He halted the eviction of the Jews and in 1615 granted them a letter of protection – the so-called Jews’ Privilege (Juden Privileg).

In today’s world, most of us are “privileged.” Privileges are little or not-so-little perks to which we feel entitled. But it has not always been this way. The term “privilege” derives from Latin privilegium, a special law applying to a given individual or to a defined group of individuals – a restricted “social contract” long before that term was invented by Rousseau. It sets reciprocal rights and duties of two parties entering into a formal relationship. Sometimes such contracts are symmetrical, often they are not; such asymmetry surely applies to the Jews’ Privilege. In fact, the German term Schutz- und Satzbrief (letter of protection and obligations) provides a better characterization of the contract. Schutz means “protection,” while Satz stands for rules of conduct and conditions. This contract offered a promise by the dominion to protect the Jews in return for the latter submitting to a set of special rules, restrictions, and obligations. It is the ultimate vestige of the earlier Imperial Servitude (Kammerknechtschaft), after it had been delegated to local rulers.

The wording of the 1615 Stühlingen Schutz- und Satzbrief would not rank highly in a literary contest. Various topics were thrown together helter-skelter, without a clear order, and phrased in nearly endless sentences without structure. To assist in the discussion to follow, and to maintain some internal thematic unity, the translated prose of the Jews’ Privilege that follows has been broken down into individual, numbered paragraphs.

Jews’ Privilege of Stühlingen, 16151

| 1. | Maximilian Hereditary Marshall at Pappenheim, Count at Stühlingen, hereby permits Phalen, Meierle, Lema, Sandelen, Jackle, Hirtzle, Costen, and Jerkuffen to reside under protection and with obligations, together with their present and future wives, children, farmhands, servants, and other members of the household in the town and village of Stühlingen, in the six houses they already own from this date for the next fourteen years. They shall be treated like his other citizens, subjects, and serfs, but be freed of forced labour, guard duty, and other civic responsibilities and burdens. |

| 2. | They are allowed all the privileges granted to them and other Jews by kings and emperors, or such privileges that are yet to be granted, as long as these privileges do not infringe established privileges, statutes, rights, and customs of town and county Stühlingen. |

| 3. | They are permitted to trade a variety of wares with inhabitants and strangers, except to sell salt or iron, or to run their own stores. |

| 4. | Under the watchful eye of the authorities, they are permitted to lend money to locals without Jewish usury and with or without usury to foreigners. |

| 5. | Any conflicts between them or with [other] Stühlingen subjects shall be settled in a Stühlingen court, and not in rabbinical or other external courts. Judges, magistrates, and other officials shall provide equal justice to Jews and subjects alike. However, the Jews shall bear the full court cost and legal fees. |

| 6. | When conflicts arise because of stolen or pawned property, the Jews shall report this to the count. They shall restore extant property to the original owner free of charge or the equivalent of the moneys loaned. |

| 7. | However, Jews are not required to return objects legitimately and transparently pledged as security for a loan, except in exchange for the originally loaned amount plus interest, according to Jewish custom. |

| 8. | Jews are permitted to live according to their laws and customs [except for access to rabbinical courts], and are entitled to perform ritual slaughter, sell ritually slaughtered meat, and hold traditional funerals [implies an already existing Jewish cemetery]. |

| 9. | They are permitted to celebrate their holidays and erect arbours [sukkoth] for themselves and with visiting Jews according to their customs; but they are not allowed to excessively shelter foreign Jews and Jewesses. |

| 10. | The Jews are permitted to have their married children live in their households or establish their own households in Stühlingen with explicit permission of the count. But without the count's permission, they are not allowed to purchase additional houses in the town or the lands of Stühlingen. |

| 11. | Like the other subjects and serfs of the count, they are permitted to visit and trade in the public market hall. |

| 12. | If the Jews bring a case before the imperial or other higher courts of appeal, then, upon request, the count will assist them like his other subjects with documents and other appropriate means at cost. |

| 13. | The count will not allow additional Jews to set up households in the county. |

| 14. | All Jews and their households are required to behave decently and not to cause any disturbance on their Sabbath. |

| 15. | No Jew shall be permitted to collect debts from the count’s subjects on Sundays. |

| 16. | They shall keep the lanes and houses clean and dispose of their waste. |

| 17. | Their wives and servants are not permitted to wash their implements, meat, and clothing at public fountains. |

| 18. | They shall not purchase defective cattle and lame horses, or let them graze on the common pasture at risk of severe punishment.2 |

| 19. | Neither Jews nor other subjects of the count shall prevent each other from either buying or selling. |

| 20. | But town and village Stühlingen shall permit each house owner to let four heads of cattle graze. |

| 21. | In return for these privileges, each of the six houses shall every Easter submit to the tax collector 10 fl. and an additional 7 fl. for imperial taxes and duties, and another 3 fl. for feed and rental of a horse. |

| 22. | Any Jew who intends to move away from Stühlingen within these fourteen years shall pay only the tax due for the actual time spent here. |

| 23. | However, Lema, Sandel, Jeckle, and Cost are relieved from having to pay protection tax for 1616. |

Berthold Rosenthal’s and Hans Brandeck’s transcripts agree practically word-for-word, except that paragraphs 20, 21, and 23 appear in Rosenthal’s, but not in Brandeck’s, version.3

Paragraphs 1, 10, and 13 delimit the terms of protection for the next fourteen years: Eight households were permitted to live in six houses they already owned. A household consists of a head, a spouse, children, servants, maids, farmhands, and other dependants. The latter often included elderly parents, unmarried adult children, and probably even unmarried siblings of either head or mistress of the household. Furthermore, the heads of household are also permitted to have their married children live with them. Given the size of families, that could have quickly led to a very crowded house. In principle, the count could permit a young couple to rent, purchase, or build their own home. But such permissions seem to have been granted rarely. No additional Jewish households will be permitted in the county. This restriction seems not to have been observed very strictly.

Formally, Stühlingen’s 1615 letter of protection applied only to the town and village of Stühlingen itself, and that was its major flaw. Scattered around Stühlingen, but mainly along the course of the Wutach River, was a series of villages, at various times under Stühlingen’s control. But during the decline of the house of Lupfen and the messy succession struggles thereafter, much of that control was lost. Already in the late sixteenth century, an extended Jewish family, headed by a Moses (Moschi), lived in Ofteringen, halfway between Stühlingen and Tiengen. They had not been included in the 1615 letter of protection. The same was true for the villages of Eggingen, Untermettingen, Lauchringen, Schwerzen, and Horheim, all places where Jews would be living over the next 140 years. Although the original letter mentioned only the village and town of Stühlingen, subsequent administrations started to manage residency permits and collect taxes from all these Jews in the absence of a firm legal basis. Whereas the number of Jews in the village and town of Stühlingen was fixed by the original letter of protection, this was not the case for Jews living in the various villages and hamlets within “Greater Stühlingen.”

Paragraphs 3, 4, 8, 11, 18, and 19 outline the Jews’ permitted sources of livelihood:Jews were permitted to trade in most goods, except for salt and iron (later also tobacco). These, as we shall see, were special monopolies under direct control of the counts. Trading in cattle and horses was acceptable, but the letter threatened severe punishment for trading in sick or defective animals. Although not mentioned explicitly, as a general rule Jews were not allowed to own a farm or to live off its proceeds.4 Jews were permitted to ply their business in the public market hall and on the road, but not in owned shops. Thus, the ability to maintain stock was extremely limited. They could sell ritually slaughtered meat. Moneylending ‘without Jewish usury’ was permitted in principle, but “usury” was not defined explicitly. In a strict sense, collecting any interest could be interpreted as usury; but what incentive would a moneylender have to accept risk without a chance at profit? An interest rate of 6% to 8% was typical.5 In fact, the records show that the lending business was brisk, despite the ever-present threat of being accused and convicted of usury. While not mentioned explicitly in this letter of protection, but borne out by the records, financial transactions (including purchases and sales) above a certain value had to be registered with the authorities.6 Jews were not allowed to pursue business on Sundays and Christian holidays. Special rules applied to the return of stolen property, whether pawned or fenced.

Paragraphs 2, 5, 6, 7, 8, and 12 address legal status and recourse: Jews were promised fair treatment by county courts and magistrates. They could appeal to the emperor for protection under the imperial servitude statute, but only as long as the issue did not contravene the interest of the count. And within these limits, the count promised to support the concerns of Jews. Of course, the count charged for any arising cost. Any conflict, whether Jew against Jew or Jew against gentile, had to be handled strictly in secular courts. Access to rabbinical courts was strictly denied, both in paragraphs 5 and 8. This was a very sensitive point. According to Jewish tradition, every aspect of life is governed by Talmudic laws. Some issues are straightforward; others require interpretation or judgment by a properly qualified rabbi. Most simple country rabbis lacked the requisite legal training, but they were still able to mediate conflicts. As shall be discussed below, the counts quickly came to regret their exclusion of rabbis for settling squabbles between Jews and relaxed this provision in the protection letter of 1671. However, there might have been good reason for their reluctance to involve rabbinical courts. Some fifty years earlier, a simple disagreement between two Jewish business partners, the financier Simon ben Elieser Ulmo-Günzburg and the printer Nathan Schotten, both in Bavarian Swabia, had escalated from involvement of a plain arbitrator, through an arbitration panel, to a local rabbinical court – with parallel involvement of secular courts – then to an open conflict between the rabbis of Swabia and those of Frankfurt,7 and ultimately it percolated all the way up to Emperor Maximilian II.8 It is thus understandable that many local rulers wanted no part of it.

Paragraph 5 clearly negates a directive from the synod of Jewish rabbis in 1603 that disagreements between Jews had to be resolved in Jewish courts.9

Paragraphs 8, 9, and 14 delimit religious practice and autonomy: Jews were permitted to live according to the Talmudic canon, including ritual slaughter and burying their dead. They were allowed to celebrate their holidays and entertain visiting Jews; but such visitors had to move on quickly, although the letter of 1615 mentioned no explicit time limit. Jews could erect open shelters for the feast of Tabernacles (Sukkoth), but they had to behave decently, without excessive noise or drunkenness. They also had to respect the dignity of gentile celebrations. This latter imposition could have serious consequences: in 1722 two Jews were fined 6 fl. for not taking off their hats on a Sunday while the church bells were tolling [R153].

The permission to sell ritually slaughtered meat created an unintended source of conflict with the local butchers. The production of kosher meat actually involves a two-stage process. The first stage, the actual killing of the animal, is relatively straightforward and can be handled by any minimally trained ritual slaughterer. The second stage, that is, removing various anatomical components that would render the meat non-kosher if left, is relatively straightforward for the front quarters of the animal, but much more complex for the hindquarters.10 Consequently, any slaughterer can handle front quarters, but the highly trained specialists that are competent to render hindquarters kosher are more difficult to find in little towns and villages. Many observant Jews abstain from eating meat from animals’ hindquarters for this reason altogether; this meat is sold to people not concerned with kosher laws, that is, gentiles. This little ritual idiosyncrasy of the Jews brought much, relatively inexpensive hindquarter meat to the general market and in turn lowered meat prices, much to the dismay of gentile butchers [R4736].11

Paragraphs 16 and 17 set standards for order and cleanliness: Houses and lanes had to be cleaned regularly. Meat, clothing, and other implements were not permitted to be washed in public wells. Waste had to be disposed properly at assigned places.

Paragraph 21 sets the protection tax: The total annual tax for each family was set initially at 20 fl. due each year at Easter. Of these, 10 fl. constituted a direct tax to the count, 7 fl. went to the emperor, and another 3 fl. covered various extra charges. These amounts must be compared with other taxes the count collected: the entire town of Stühlingen had to submit 10 fl. per year, the village of Stühlingen 12 fl., the villages of Schwaningen and Mauchen 4 fl. each, Lempach and Weizen 3½ fl., and Eberfingen and Eggingen 2½ fl.12 In other words, the annual tax of each Jewish family to the count was as much as that of all the citizens of the town of Stühlingen together.

Protection taxes in the early modern period were collected in two different fashions depending on the municipality. Often Jews were responsible individually for paying their family’s tax directly to the tax office (Rentamt). This was the case in Stühlingen; in other jurisdictions, the Jewish community had to pay their taxes collectively. Either the rabbi or the community trustees (Parnas, Barnosse) were charged with collecting the taxes from the community members, often according to their ability to pay.13 A rare mixture of these two fundamental tax collection policies is found in some Bavarian communities, such as Floss and Hürben.14 There, the Jewish community was, from the standpoint of tax collection, divided into two subgroups. The first, called ‘the conditional twelve’ (bedingte Zwölf), were taxed collectively; they constituted essentially the first-born descendants of the first twelve Jewish families in the village. The second group, called ‘the unconditionals’ (unbedingt), were taxed individually. Belonging to the first group seemed to have been socially desirable, for unconditional Jews clamoured to move into the conditional group whenever a slot became vacant, despite a higher average tax burden.

Why would the wealthier Jews agree to a scheme that taxed them more severely than their less well-off brethren? Sociological research demonstrates a distinct benefit of ethnic concentration.15 Such an advantage of concentration may well have motivated the wealthier community members to take on a higher share of the tax for everyone’s benefit. However, excessive ethnic concentration invites hostility from the host population16 and thus again threatens social stability.

Taxing each Jew individually according to a fixed schedule could lead to serious hardships for the poor. Occasionally, the authorities would show some leniency. Yochanan (Hönlin Y1), a poor religion teacher, had his tax set originally at 10 fl. When he could not pay that much, it was reduced to 5 fl., and in 1668 he did not have to pay tax at all, ‘as long as he would not engage in any commercial activity’ [R4186]. The tax was also forgiven occasionally for poor widows and very old men. But conversely, Jews could be evicted if they became unable to pay their tax. This was the fate of Joseph Gugenheimb, Sandel’s son-in-law, who had to leave Stühlingen in 1739 and move in with his son, who lived elsewhere [R1144].

The 1615 letter pays no attention to the internal organization of the Jewish community. The appointment of neither rabbis nor community trustees (Parnas) requires confirmation by the authorities. In fact, neither cantor nor beadle (Schulklopfer) were even mentioned. Thus, secular documents are relatively silent regarding internal aspects of Jewish community life.

When compared to other seventeenth-century letters of protection, the 1615 Stühlingen Jews’ Privilege is relatively simplistic, lacking many elements found elsewhere, and rarely considers the law of unintended consequences. It is closer in character to the individual letters of protection from earlier periods. Terms of dismissal from protection are not discussed; wine and other alcoholic beverages are not mentioned. Usury is not defined. Timing and procedures for renewal of the letter are missing.

Mordstein has provided us with a useful multistep method for analyzing letters of protection and their impact:17

In other words, a letter of protection does not exist in a vacuum. First, there is the intent or purpose for which the letter is issued, which determines the actual wording of the letter that defines privileges, limitations and taxes. These are then operationalized as written bylaw or regulations. And finally, officials have to implement the regulations. Problems can result from issues at any stage.18

We know next to nothing about the intent of Maximilian von Pappenheim or about any negotiations with the targets of the letter. It makes sense that some kind of written regulations existed, but as yet they have not been found.. A bylaw requiring the recording of financial transactions probably did exist, for financial transactions are on record, and such records are not explicitly mandated by the letter proper.

It does not appear as if the Jews had any control over who was to receive a letter of protection and could take residence in Stühlingen. These decisions were made by the rulers and officials [R945].

Overall, one does not get the impression that the 1615 letter of protection for the Jews of Stühlingen was the result of careful analysis and planning. This is not surprising. Its major goal was to retain the Jews as a valuable source of taxation and credit. In fact, Maximilian was in dire financial straits. The initial purchase of title and county through Maximilian’s father, Conrad, resulted in a considerable debt burden. The cost of maintaining a suitable lifestyle with two households, one local, the other in the imperial capital Vienna, added further to the problem. In 1613 he had to sell extensive landholdings in the Black Forest19 for 88,500 guilders, and in 1621 the Gräfenthal county in Thuringia, which he had inherited from his uncle Christoph Ulrich von Pappenheim in 1599 for the sum of 130,000 guilders.20

Maximilian von Pappenheim continued to collect various taxes from his Jewish subjects and pro forma serfs until his death on February 14, 1639. His first son, Ernst Friedrich, had died in infancy. His second son, Heinrich Ludwig, was killed in the Thirty Years’ War during the siege of Castle Hohenstoffeln by a shot to the head in 1633. His daughter, Maximiliane Maria, died as the young wife of Count Friedrich Rudolf von Fürstenberg in 1635; the widower thus inherited the title to Stühlingen town and county on behalf of their young son.

Protection and tax demands continued under Fürstenberg’s rule, but no new letters of protection were issued for the next fifty-four years.

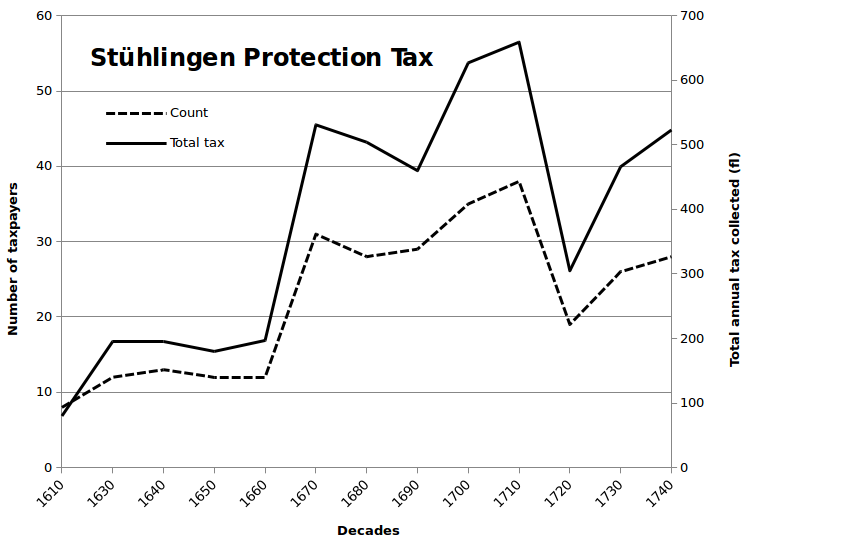

The data for the diagram in figure 6 has been collated from the various municipal and county records. Since the archival holdings are incomplete, taking averages would have underestimated the actual taxes paid; instead, we have chosen the maximum annual value in each decade. It thus appears that the taxed Jewish population of Stühlingen was relatively stable until the 1660s. It then rose rapidly over the next ten years, partly due to coming of age of the third generation, and partly due to immigration, possibly as an after-effect of the Thirty Years’ War. The majority of new taxpayers settled in the surrounding villages, but were taxed by the counts of Fürstenberg, and administered through Stühlingen. Their number exceeded by far the original number of contractual slots. The gentile population of Stühlingen objected vigorously, and in 1671 a new letter of protection was issued that attempted to stem the growth. This letter set the number of protected Jewish households at thirteen plus, at most, one married child, that is, a total of twenty-six households, as well as a cantor and a beadle (Schulklopfer). No allowance was made for a rabbi. For the new letter of protection to be issued, the Jews had to make a one-time payment of 500 fl., and in addition the Jews had to assume a debt of 500 fl. to the count. The annual protection tax was raised to 18 fl. plus a plump goose per household.21 Although the number of Jews stabilized, popular complaints persisted [R1281].

The Jewish population remained relatively stable for another twenty years, but then started to creep up again. The next letter of protection was issued in 1696 for thirteen households in the town, plus five households in surrounding villages (each with a married descendant). This time, the one-time payment amounted to 1500 fl. plus the assumption of another debt of 500 fl. to the count and a disbursement of 150 fl. as “interest.”22 This new protection was followed by another growth spurt, cut short by the expulsions of several Jews, some because they could not pay their taxes, some for transgressions, and some without explicit reason. This expulsion is referred to bashfully in the tax collection record Easter 1717:

Protection tax of the Jews, each 10 fl. On Easter 1717 in Stühlingen from Leib Jud, Marum Weyl Sandels son, Salomon Weyl, Meyer Menckin son Bloch, Mausche old, Joseph Marums son, Lemble old, Schmule Seeligmann, Meyer Lehemann Bickert, Isac Abrahamben son, Joseph Sandels son-in-law, Jonas Models son (has moved away, therefore null), Hirtzel Isac Son (regular null), Faissel Leiben son, Mausche Models son (also gone and null), Josell Lang Schmule son, Marum Lemblin son (has left regularly, null), Menckin Bloch, Lehemann Bickert, Elias Jud, Israel Meyer, Jonas Leiben son, Daniel Bickert (has moved away, null), Jäckelle Hirtzels son von Eberfingen, von Horheim Davidt Jäggelin son (also null), Menckin Bernheimb, Meyer Bernheimb, Elias Boll (null), Jüdelle Weyl, Isac Bernheimb Beniamin son, Menckin Meyer, Meyer Weyl Jüdelin son. [R542]

The issue of the final protection letter of 1717 did not proceed without some disagreement. The Stühlingen citizens demanded an end to the letters of protection.23 The underage prince Joseph Wilhelm Ernst von Fürstenberg-Stühlingen, having had a strict Jesuit upbringing, was fiercely opposed to another twenty years of Jewish presence in Stühlingen. But with the support of the abbot of St. Blasien, he was overruled by his legal guardians.24 It was argued that the local citizenry collectively owed the Jews as much as 30,000 fl., an amount that could not be repaid on short notice. When Wilhelm Ernst Joseph assumed the throne in 1723, he condescended to extend the protection once only for thirteen families under new conditions and another one-time payment of 4000 fl., plus another 50 fl. per household.25

It is important to note that the total tax count indicated in figure 6 refers to households, not to individuals. Since a household commonly comprised husband, wife, children, senior or unmarried relatives, and servants, the actual number of Stühlingen Jews in, for example, 1710, could easily have exceeded two hundred souls.

The protection letter of 1671 modified the 1615 conditions as follows:26

| 1 | To save the secular officials from being inconvenienced, rabbis were now permitted to mediate in internal quarrels between Jews. |

| 2 | Because, in the past, the Jews had concealed all kind of undesirable rabble, beggars, criminals, and other visiting relatives, from now on itinerants could be hosted for only one night or over Sabbath. |

| 3 | Whenever the count’s household or his officials required horses, the Jews had to supply those for free. |

The protection letter of 1696 imposed further changes:27

| 1 | Half of any fine imposed by a rabbi for any reason had to be delivered to the civil authorities. |

| 2 | Houses could be bought or built by Jews only with explicit permission by the authorities. |

| 3 | Property acquired by Jews on auctions had to be resold to gentiles within twelve weeks. |

| 4 | Jews had to contribute to the war debt imposed on the county (no explicit amount mentioned) |

| 5 | Jewish households were exempted from having to billet foreign soldiers and could substitute payment instead. |

| 6 | The requirement for the gratuitous provision of horses to officials was discontinued. |

| 7 | The Jewish community could apply to the authorities to have an uncooperative member evicted. |

| 8 |

If due to war and other conflicts the Jews were temporarily deprived of their protection, the authorities could consider a partial return taxes paid. |

Considering that the Jewish community could not come to an internal agreement about providing horses for official tasks, they have been grouped into three categories. Category one is to provide three horses in turn and includes Leib Gugenheimb and Marum Weyl. Category two provides two horses and includes Joseph Gugenheimb, Salomon Weyl, Mayr Bloch, Faistel Gugenheimb, Jonas Gugenheimb, Isaac Bikhert, Lehemann Bikhert, and Elias Mayr. Category three provides one horse and includes Joseph Gugenheimb Sandels Tochtermann and Schmule Weyl Lemblins Sohn. With details about their duties (horses on which an honest man will not break his neck). Whoever does not own a horse is to borrow one [R3008].

Only two of Stühlingen’s Jews on protection that year did not have to provide horses at all: Lemble Weil, who must have been about eighty years old, and Lang Josel Gugenheimb, whose financial difficulties were well known [R3061]. The decree suggests that a transparent economic stratification existed within the Jewish community, and the additional economic burden was distributed according to a quasi-modern, ‘progressive’ tax system.

In the end, the 1717 letter of protection made life for the Stühlingen Jews very difficult:28

| 1 | The inclusion of a married descendant in the protection was abolished, which led to a major emigration of married sons and son-in-laws with their families. |

| 2 | Jews were only allowed to trade in textiles and leather goods manufactured in Stühlingen. |

| 3 | Cattle bought by Jews outside the Fürstenberg dominion required inspection and a certificate of health by a local farrier before they were allowed on local pastures. |

Thus, the existing conditions had progressively tightened to the point where the final act of eviction in 1743 came almost as a relief.

Footnotes -> List of References

1FFA, Judenakte, Politica, Amt Stühlingen, giv. I, subdiv. 1, Die Annahme der Juden 1615–1784.

2It would be more logical if Jews were forbidden to sell defective horses; “purchase” might be an error in the original text.

3Rosenthal, Heimatgeschichte der badischen Juden, 75; Brandeck, Geschichte der Stadt, 87.

4Mordstein, Selbstbewusste Untertänigkeit, 227 - 239; Ullmann, Nachbarschaft und Konkurrenz, 379.

5Mordstein, Selbstbewusste Untertänigkeit,.228 - 242.

6Ibid., 229

7Rabbi Eliezer ben Naftali Herz Treves, whom we have already met in the previous chapter, served n the rabbinical panel of Frankfurt. It is likely that his printing expertise was relevant in regard to the Burgau printing enterprise.

8Rohrbacher, “Ungleiche Partnerschaft,” 204.

9Zimmer, Jewish Synods, 192.

10Zivotofsky, “Tzarich Iyun.”

11Mordstein, Selbstbewusste Untertänigkeit, 241.

12Brandeck, Geschichte der Stadt, 133.

13Mordstein, Selbstbewusste Untertänigkeit, 302; Ullmann, Nachbarschaft und Konkurrenz, 107.

14Höpfinger, Die Judengemeinde von Floss, 53; StAA, VÖ, lit. 240, Urbarium der VÖ, Herschaft Hürbi, fol. 108r.

15Driedger and Church, “Residential Segregation,”

16Quillian, “Prejudice as a Response,”

17Mordstein, Selbstbewusste Untertänigkeit, 257.

18Mauerer, Südwestdeutscher Reichsadel,

19GLA, 109/502.

20Warlich, “Fürstenberg-Mößkirch.”

21Häusler, Stühlingen: Vergangenheit und Gegenwart, 155.

22Ibid., 156.

23Rosenthal, Heimatgeschichte der badischen Juden, 173.

24Samuel Pletscher Collection 1610;

25Häusler, Stühlingen: Vergangenheit und Gegenwart, 157.

26Rosenthal, "Heimatgeschichte der badischen Juden," 172.

27Ibid.

28Ibid., 173.

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.